Fintech App UI/UX Design Guide: 15 Tips to Fix User Journey and Experience

Aramide Ogunbewon

Brief History of Fintech

The fusion of finance and Technology has changed what we know as sending and receiving money to encompass money creation, management, and multiplication. Fintech had its first global imprint through the need to send money across countries during the popularization of digital technology in the late 20th century.

The late 1990s saw the use of the Internet, which led to the use of online banking and the establishment of early finance companies like PayPal. Then, in the early 2000s, digital currencies like E-Gold and Bitcoin emerged. This brought the concept of decentralized finances and every other related aspect of fintech.

Types of Fintech

Digital Banking: It allows users to make transactions with mobile devices and access the Internet. Many traditional banks have shifted from paperwork to serving their customers with services such as opening an account, sending and receiving money, making bill payments, offering loan services, and offering other self-services to manage their accounts. E.g. UPI apps, bank apps like Canara, HDFC bank app.

Saving/Investment: Fintech solutions provide real-time tools and platforms for individuals to save and invest their money. They have features like automated investing, micro-investing apps, and peer-to-peer lending. These products come with dashboards and analytics tools to help give users data to make financial decisions.

Cryptocurrency: This technology uses digital assets and currencies for investment and is secured with cryptography. It has become an acceptable payment form in the US and other Western countries. The security system does not allow for a single central authority; hence, it uses a decentralized network to serve users.

Blockchain: Like crypto, blockchain is a decentralized technology that keeps records of transactions across various networks in a way that cannot be destroyed without the owner’s consent, which is a part of the smart contract.

While blockchain can store data on content across various industries, it was popularized for its security in keeping and aiding financial records. Many people now leverage blockchain to create, sell, and maintain digital and physical assets. The transaction of these assets is made possible through cryptocurrency. The most popular product is the Ethereum smart contract.

Currency Exchange: Technology has also helped improve the quality of services for currency exchange. It involves a lot of global politics and economics, which means a lot of legal restrictions, which has made international trade difficult.

Fintech has helped manage many problems, giving customers a more seamless and accessible experience in exchanging currencies. It has also removed the monopoly of exchange rates from traditional banks. E.g. Wise, Paypal

International Payments: This is one of the problems caused by restrictions in currency exchange. Fintech products have assisted in reducing processing times for cross-border transactions, lowering service charges, and increasing transparency in handling customer funds. Popular examples include Paypal, Payoneer, and Stripe.

Neobanking: This is similar to digital banking; it relies primarily on using digital devices to perform transactions. Digital banking can still use the traditional system to offer various financial services to their customers. Still, neo-banking is strictly an online interaction between the bank and its customers through a website or mobile app. UPI apps are perfect examples of neo-banking; even traditional banks like HDFC are now integrating UPI into their banking system

Fintech SaaS: So many financial institutions and service providers need other technological solutions to help improve the delivery of their services to their customers, and that’s where SaaS come in.

They usually offer cloud-based services, scalable solutions, and cost-effective methods of managing employees or financial services for end customers. However, they are not very popular with the average user as they do not offer direct services to customers. Examples are Shift, Stripe, and Klarna.

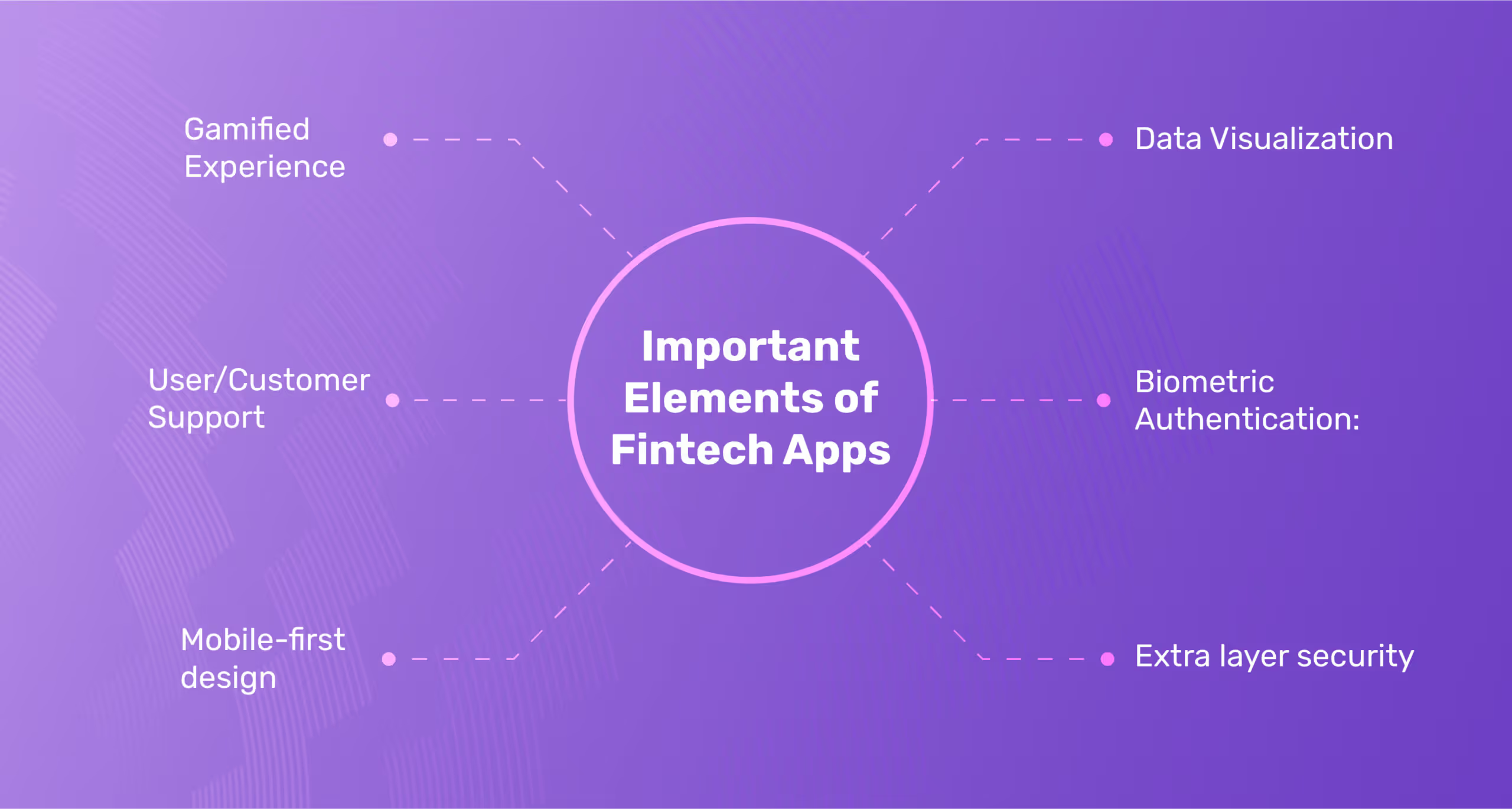

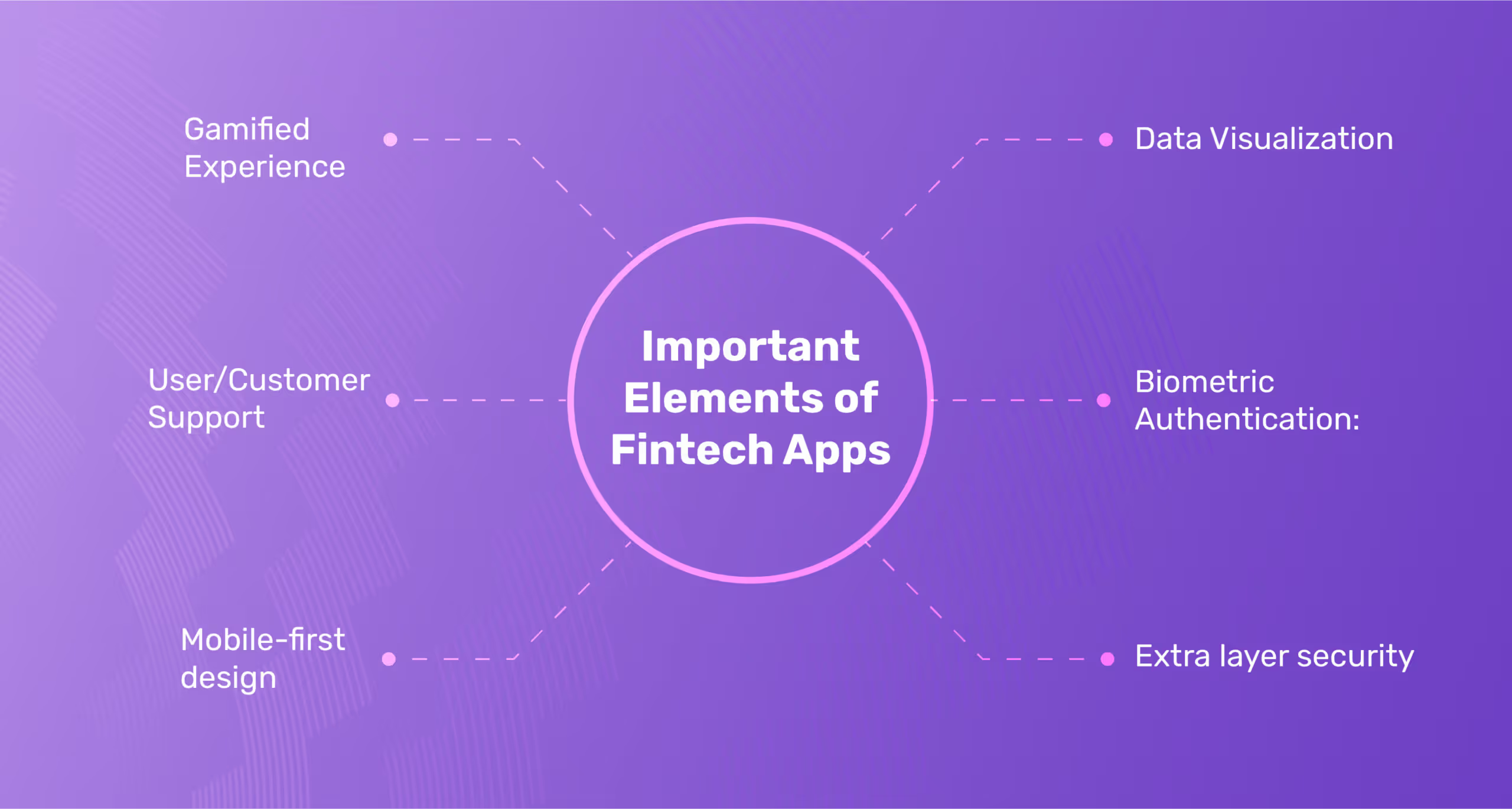

Important Elements of Fintech Apps

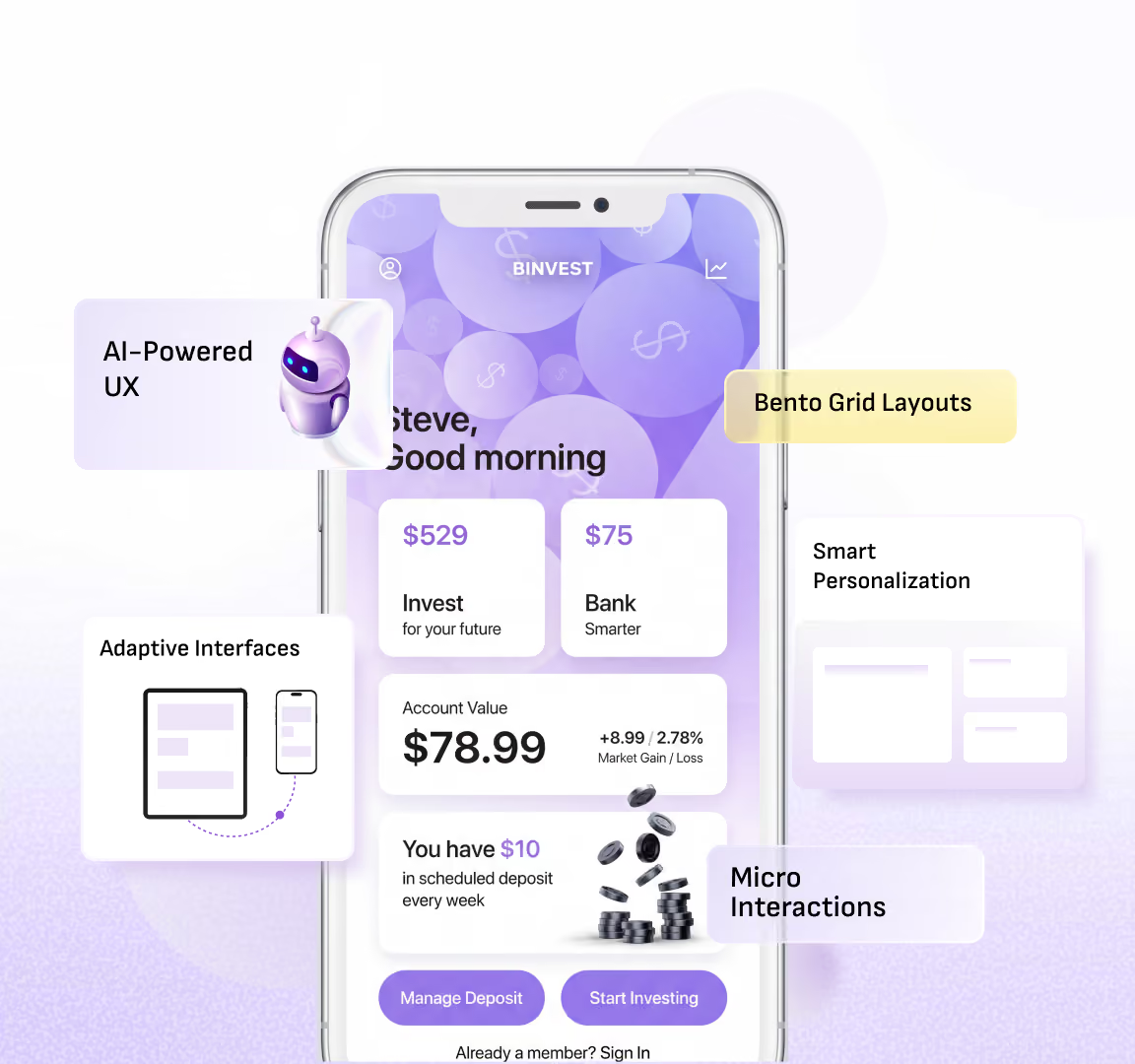

- Data Visualization: Fintech products involve figures, which can be mentally taxing for users to remember figures and statistics. This is why it is impossible to remove visualisation from Fintech designs.

Users need to manage their dashboards, wallets, or portfolios, as the case may be. The usability of such a service thrives on the availability of good data visualization. For instance, a budgeting app should feature charts and graphs showing spending habits over time.

- Biometric Authentication: The same level of privacy given to a smartphone is the same level of privacy that should be accorded to Fintech apps. If biometric authentications are available on smartphones, why not fintech apps?

Fintech apps should incorporate this to give users a sense of security and privacy while using the app or website. However, this should not be intrusive, like making the camera active during transactions.

- Extra layer security: Cybersecurity is a top priority in the digital age, where user experiences (UX) are crucial in determining the success of goods and services.

Fintechs deal with people’s hard-earned money and financial assets. A cybersecurity lapse can cause irreparable damage to the user and the service providers. Fintech product owners should prioritise the data integrity of their users without compromising usability to give a delightful and secure user experience.

- Gamified Experience: Fintech products are usually seen as rigid and too formal, which can be monotonous for users. Incorporating game-like elements into the app will make it more engaging and fun, leading to increased conversion.

It can add value to the user experience besides the conversion and business goals. It serves as a source of motivation for users to interact with the app more frequently and achieve financial goals.

- User/Customer Support is the bare minimum for any fintech or edtech product. A functional customer support system should respond quickly to user queries. It can be an AI Chatbot, FAQs, live chats, Video tutorials, or support ticketing. This system builds trust and loyalty and helps users resolve issues quickly.

- Mobile-first design: Mobile apps are easier to use and navigate than mobile websites. Marketing Dive reports that 85% of mobile users prefer apps over mobile sites, which also results in a higher conversion rate on the platform.

Users would rather use their mobile phones to perform transactions for security reasons. Therefore, it makes sense to provide them with an optimized mobile experience so that they can continue using the product.

The Future of Fintech Apps

As the fintech industry is booming, the use and misuse of it are also rising. There will be a proliferation of products, which will lead to competition. New technologies will emerge to make sure the market is sustainable. Let’s have a look at the major future trends in the fintech industry,

Artificial Intelligence

AI has been in the ecosystem for a while, but its potential has not been fully utilised, especially in fintech. There is more to AI than our eyes can see, so designers should consider this to hone their craft.

For instance, AI can be used for fraud detection. Designers should find a way to incorporate fraud detection with AI to keep users cyber-aware. Artificial intelligence should complement their problem-solving and creative skills to design financial experiences.

Blockchain

As mentioned earlier, blockchain offers a transparent and immutable record of financial transactions. Smart contract technology can improve the quality of loans or insurance services by eliminating the back-and-forth during lending and repayment.

Video Banking

This is an undiscovered goldmine in fintech. The emergence of neobanking will give rise to video banking, so designers should be futuristic in their idea/solution generation. Video banking allows customers to interact with bank representatives remotely, giving them a convenient, accessible, and personalized experience.

Digital assets

Fintech start-up owners should be ready to diversify their portfolio beyond physical currency and assets. Cryptocurrencies are already accepted as legal tender, and people are pushing for Non-fungible Tokens(NFTs) representing digital art to be legalized. All these and more can be tokenized and used as a store and measure of wealth.

Sustainable Banking

Green campaigns are penetrating every industry to reduce the effects of climate change and global warming. As sustainable practices become a unique selling point for many brands, UI/UX designers must consider how to incorporate them into fintech products.

Designers can introduce tools and features to help users invest in environmentally and socially responsible companies. It can be in the form of a carbon footprints tracker that provides recommendations for reducing its impact.

Strict Regulations

Digital technology and the Internet have shortcomings, including unrestricted access to information. This can damage data privacy and security, which will also affect fintech. Designers and fintech startups must take strict measures.

Government policies might not also affect the business operations of many fintech products. It is important to watch for policies that can be limiting and find a solution promptly before they start affecting users.

Internet of Things

Beyond the screen, the finance industry already has physical products, but with the rapid advancement, there will be a greater demand for products that will help users maintain their financial health.

This should prompt designers to upskill their games and look beyond pixels and frames. They should see how digital financial services can complement physical devices to give an intuitive and amazing experience. For example, a device can collect data on spending habits or help trigger automated payments.

Problems of Fintech Apps

Slow Load time

Time is of the essence in fintech, and most fintech apps take a long time to load. Users trust these apps with time-sensitive transactions, such as buying stocks, investing in IPOs, paying bills, and making other forms of investment where it’s a matter of time before the user gains or loses money.

Users complained that they were saving money to invest in a certain asset when the time came, and the app stopped working due to peak-hour traffic. The investor lost the opportunity to do so and got frustrated, which can lead to a loss of trust.

According to Google studies, one out of two people expects a page to load in less than two seconds. Yes, we know it’s shocking, but if you also expect Figma to load in two seconds to meet the deadline.

Possible reasons:

- Slow load times often result from unoptimised code

- Overloaded servers

- High traffic volumes during peak hours

Possible Solutions:

- Fintech apps should invest in technologies like content delivery networks (CDNs)

- Make sure that the server infrastructure is top-notch

- App designs should be lightweight

- Conduct load and stress testing to ensure the app can handle increased user numbers.

Offline access

Fintech apps are all online, and you may think the internet is widely available to everyone, but you will be surprised to know it’s not true. Only 66.2% of the world’s population has access to the internet; consequently, the rest of the population does not have access to the internet and, hence, digital banking.

The absence of offline access to fintech apps may not seem like a big issue to you (people with internet) as you scan and pay within seconds until you meet the six million unbanked Americans.

These and other people who don’t get to use the internet at all times of the day and year should get offline access to fintech so that they feel they belong to the civilised world. Fintech apps depend on the internet and telecoms for connectivity, and it’s a big restraint.

Possible outcomes:

- Not being able to use fintech apps in the time of emergency because of connectivity issues

Possible solutions:

- Fintech companies should integrate features like data synchronisation. This allows users to view and interact with basic features even offline, and updates occur automatically when the app regains internet connectivity.

- A prepaid card-based solution provider is testing a new product that uses NFC technology with a Fintech player. Customers can pay for transit services like buses and metros in cities by swiping their cards over NFC-enabled PoS devices. The solution can also be used as a wallet to pay merchants at select shops.

Poor accessibility

Accessibility refers to people from all arenas with different capabilities who can easily and intuitively engage with financial services and technology. It includes people from all walks of life, such as people with physical accessibility, digital literacy, and the availability of services to diverse groups. No matter how much fintech is on the rise, without accessibility, its deployment will never be done efficiently.

People who need to be considered while designing for inclusivity are:

- Older adults who find it challenging to adapt to new technology

- Disabled people with visual and hearing impairments

Possible outcomes:

- Inadequate accessibility risks non-compliance with global standards like WCAG (Web Content Accessibility Guidelines).

Possible solutions:

- Simplifying user interfaces and providing targeted support can bridge this gap for older people so that they don’t feel overwhelmed and excluded

- Incorporate features such as screen readers, voice commands, adjustable font sizes, high-contrast themes, and customisable settings.

- Fintech companies should invest in educational initiatives that empower these demographics. Partnering with community organisations and leveraging local resources can enhance digital skills and build trust in new technologies.

- Providing multilingual support

Security concerns

Security is paramount in fintech apps because who wants to share their financial data in this economy? Financial data is sensitive due to recurring data breaches, phishing attacks, or unauthorised access to accounts.

Possible reasons:

Some fintech apps have weak encryption protocols, inadequate multifactor authentication (MFA), and outdated security patches, which can cause users to have security concerns.

Possible outcome:

The outcome of breached security can be harmful in many ways, such as financial fraud. Even fintech companies can face legal consequences and penalties, and their reputation in the market can be damaged.

Possible solution:

Fintech companies should strictly follow security measures such as:

- Biometric authentication

- End-to-end encryption

- 256-bit AES encryption

- Notifications about all actions

- Real-time fraud detection.

If a fintech company wants to be hack-proof, it must conduct regular penetration tests after each new update and integration.

Hidden Fees and Charges

Fintech businesses should thrive on transparency, and hidden fees are not proof of transparency. Many fintech apps in the market boast about being cost-effective and even free when users try to use a service, fees that were undisclosed before flashing on the screen, which puts them off.

Businesses may refer to these fees as transaction charges, account maintenance charges, currency conversion costs, or subscription costs. These fees are usually revealed only after the user completes the transaction, so they have no chance of returning.

Possible outcome:

Encountering hidden fees while trying to use a service can create a negative impression in the user’s mind, eroding trust.

Possible solution:

Fintech companies should be upfront about their pricing structure so that users don’t eventually face a surprise (rather a shock). A detailed breakdown of charges helps create an environment of transparency.

Too many services

Most fintech businesses offer various services under one platform. While a one-stop destination for all the services may make sense, catering to such a wide audience may also fail terribly.

Possible outcome:

Fintech businesses typically offer numerous services, such as investments, loans, payments, UPI, and financial planning. However, too many services in one platform can overwhelm and confuse users, as the interface becomes cluttered and users can’t find the features they need.

Possible solutions:

Fintech companies should opt for an intuitive design and try to make the user journey as personalised as possible. Customisable and segmented dashboards can enhance user experience by preventing feature fatigue.

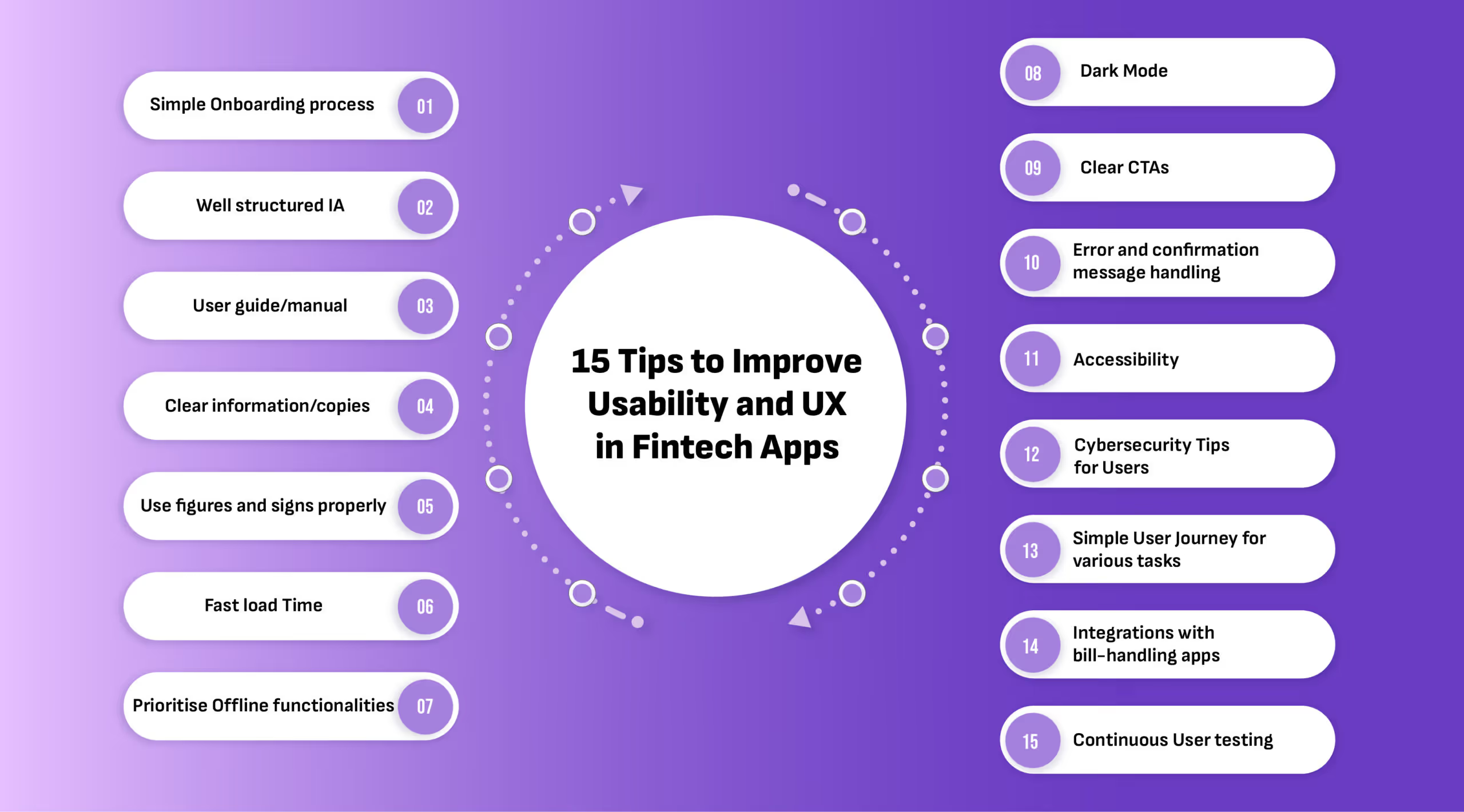

15 Tips to Improve Usability and UX in Fintech Apps

This is a detailed breakdown of tips for ensuring your FinTech design is functional and usable. Whether you are a designer or own a FinTech product, consider these tips when making design decisions.

Simple Onboarding process

When designing the onboarding process, keep people’s attention span in mind. It is very short, so don’t ask them to fill out gazillions of blank forms before they can check their balance or make a quick money transfer.

That’s because people usually leave the process in the middle and decide to return when they have enough time and energy, and that time almost never comes.

While designing the UX of a FinTech app, the login page must be designed so that users find it easy and engaging to access the app without compromising their security.

Many users have said biometrics is the best and quickest way to log in. Unfortunately, not all businesses have the technological means to offer this feature.

Well structured AI

Information Architecture lays a solid foundation for any design. Any problem or underlying issues at that stage will lead to usability issues when the design is completed. So, designers should solve any issues early enough.

How do you create a well-structured IA?

- Build a content bank and arrange all content in a logical way

- Each content should flow to the following content seamlessly

- It is okay to repeat similar navigation like CTAs, buttons, frames

- The pattern of arrangement should also be similar

User guide/manual

Have you ever bought an appliance without a manual? If yes, what did you think of the product? It was fake or stolen. The same psychology can be applied to digital products. There should be a guide for users, especially new users. Similarly, the guide should be handy in the app’s settings.

The guide should contain the following information:

- How to use the app for the first time

- Explanations of the features

- How to make enquiries/complaints

- Tips for safeguarding against financial crimes

- Use screenshots, diagrams, and videos to illustrate complex concepts.

This would reduce churn rates and support tickets.

Clear information/copies

The fintech experience relies heavily on information to avoid financial blunders for users. So, it is imperative to pay proper attention to UX Copies. Hire a UX Weiter with a background in finance and technology. This way, the copies will be intuitive and complement the design.

UX Copies should be:

- Short

- Scannable

- Concise

- Consistent in tone

- Empathetic

Use figures and signs properly

In fintech, we deal with numbers, stats, and figures. Signs and symbols are appropriate only if they are used with the intention of not causing havoc. For instance, a fintech start-up in India should prioritise using the rupee sign over the dollar sign to denote the currency. It is easier for Indian users to get a whiff of their assets in lakhs and crores rather than in hundreds of thousands.

Also, make sure that icons representing something are consistent throughout the design so the users won’t be confused. The use of colours can also help convey important messages without excessive explanation. For instance, red is a warning sign. Designers can include features that allow users to set a threshold for warning when their asset drops below the threshold.

Fast load Time

Users do not want to waste time on sending or investing, so they switched to digital mode; otherwise, they would have chosen to stick with queuing at the bank. With the advent of short-span content, people now have the attention span of a goldfish. They don’t want to wait even for a few more seconds. They will opt for another option!

To improve your fintech product, you should focus on

- investing in technologies like content delivery networks (CDNs)

- Use quality server infrastructure that can cater to a large number of users

- The design should be lightweight and simple

Prioritise Offline functionalities

Understandably, transactions cannot be made without access to the Internet, but other tasks can be done without access. Core features like account balances and recent transactions should be accessible offline for their perusal.

You can then display a message to them that they are offline and that their data will be synchronized when they go online. It’s easy peasy.

Dark Mode

Digital technology has brought about increased screen time. This has both physical and mental effects on individuals. UX designers should act as the guardians of digital interactions to reduce the strain users experience due to excessive exposure to blue light.

Dark mode is here to stay. Its benefits range from less eye strain to the fact that it looks much better on modern OLED screens, where the blacks are accentuated.

- Dark mode reduces the amount of blue light emitted from the screen, making it easier on the eyes, especially in low-light conditions.

- It can improve readability, especially for users with visual impairments.

- Remember sustainability? Dark mode can help you achieve that. It conserves battery life on devices with OLED screens.

Clear CTAs

CTAs are one of the micro-interactions in a design, and they can easily get lost among so many other elements. If CTAs are not noticeable, what will make users take action? How will you increase conversion?

A call to action (CTA) is a prompt on a website that notifies the user to take a specific action. Without an apparent CTA, the user may not understand the next steps to buy a product or sign up for a newsletter and will likely leave the website without completing their task.

You can incorporate this to ensure your users find the product easily:

- CTAs should be easy to locate with brighter colours and animations or placed in the middle of the screen.

- They should not exceed 3 to 4 action words.

- They should be consistent in how they look and behave throughout the design.

Error and confirmation message handling

Error and confirmation messages personalize the user experience and give the user a sense of direction in completing their task. People do not joke about their finances, which raises suspicions that a fintech app or website does not provide feedback, especially when a transaction is completed successfully or unsuccessfully.

- Errors should be clear enough; there is no need to sound too emotional if a transaction fails to reduce the probability of confusing the user.

- The error message should not just notify; it should give a next step. It could tell them to wait 10 minutes and try again or contact the support team.

- Confirmation messages should also be simple and engaging, using icons, sounds or animations.

Accessibility

What’s the point of designing a digital product, be it a website or app, if it’s unavailable for everyone? To improve usability in a fintech app, ensure the application is universal regardless of the user’s age, gender, and ability.

A business’s success is more likely when the audience base is wide. By bringing accessibility into the scene, inclusivity comes along, which broadens the user base. When a web page can be used/read and understood by a wider range of people, including those with cognitive disabilities, it is said to have an accessible design.

You do this by:

- Ensuring there is sufficient contrast between text and background. Use this colour contrast tool.

- The fonts should be legible and readable; avoid cursive fonts in fintech designs.

- Your design should be compatible with screen readers.

- Give users options to customize their page.

Cybersecurity Tips for Users

A well-designed user interface (UI) can positively influence user behaviour, making it crucial to integrate security measures seamlessly. A fintech design should be the agent of change in teaching users about cybersecurity.

You can include a short description of why users should protect their account balance or include cybersecurity tips in the FAQs or help and support. More tips for your users include

- Encouraging them to use multiple characters for passwords

- Implement multifactor authentications

- Remind them to update their software Regularly

Simple User Journey for various tasks

Many designers confuse the app with a maze, and they design it so that it becomes a task for users to find the feature that they want to access. They have to open all the categories and subcategories and break through them to find the one feature they seek.

One of the main goals of the user experience design in finance is to help your customers achieve their goals as quickly and effortlessly as possible. Here, it’s important to evaluate whether your financial app might remind users of a jungle. If so, a careful UX audit and evaluation of all the functionality should occur occasionally.

Often, users only use one-third of the functionality available. Removing unnecessary functions transforms the service’s experience into a much more pleasant one.

But, as we are talking about smart changes that can be done quickly and have a great impact, you should focus on at least guiding the users through the jungle with helpful navigation.

- Minimize the clicks.

- Progressive disclosure: reveal what is necessary one at a time.

- Make the navigation intuitive

Integrations with bill-handling apps

This is very important for regular banking fintech. The aim is to make transactions easier and faster, right? It makes sense to do that by integrating the billing service/product they are already used to.

Everyone recharges their data, pays taxes, pays electricity bills, has insurance, etc. Leverage the common services they purchase and integrate them without overcrowding the app. Allow them to pay their bills with auto features or, better still, send reminders and notifications for upcoming bills so they do not lose track.

Continuous User testing

After implementing all the above tips, nothing beats knowing the users’ minds. Unlike the aforementioned tips, which can be done once or twice, user testing should be done from time to time. There are various ways to inquire from the users:

- Usability Testing: Usability testing helps identify pitfalls and errors in product use. The main ingredient in conducting these tests is empathy.

- A/B Testing: This method involves conducting a test with different design variations to identify the most effective solution for users. It is sometimes referred to as bucket testing or split testing.

- User Interviews and Surveys: You should conduct interviews and surveys, whether physically or online, to learn what the users think about the product and how it can be made easier for them. The interviews should be adequately planned to uncover the real issue.

Fintech Case Study

It is one thing to understand the theory of a concept; it is another thing to know how theory comes into play in real-life products.

Paytm Paathshala

Paytm Paathshala is one of a kind in revolutionizing how trading is taught. Learning to trade in foreign currencies or crypto can be demanding and sometimes too technical. As a result, Learners often leave the journey halfway through, which is a problem in the industry.

Problem

- There is low awareness about financial literacy and education. People think finances begin and end with saving and spending.

- Teaching about finances in the regular school setting is ineffective and inefficient.

- Users can interact and engage on the platform.

Solution

YellowSlice brought its expertise by redesigning the Paytm Paathshala app to make learning as effective as possible.

- One of the tips for Fintech is Gamification. This helped to reduce the feeling of boredom among learners.

- Gamification also increased the awareness of trading and investments through several games.

- Quizzes and puzzles were introduced to test the effectiveness of the learning and identify areas in which the users need to improve.

DRIP Capital

Drip Capital is a fintech company that provides financing solutions to small and medium-sized businesses (SMBs). YellowSlice redesigned the web portal to enhance the user experience for potential customers and existing clients.

Problem

Fintechs thrive best for their credibility; one crucial thing that improves credibility is a proper design system. The lack of a design system made the design look outdated. The design system would also create a scalable design to create more pages and features in the future without the need to overhaul the whole design.

Solution

- First, a stakeholder workshop was conducted to understand the vision and goals of the business.

- The next phase was to understand the extent of innovation, so the YS team conducted an audit of the previous website. It also created a base for the portal designs without ruining the branding structure.

- YS created a detailed design system for them, allowing easy and simple information architecture.

- We created a sample design and conducted user research. The feedback was crucial in determining the best design to work with.

- Another deliverable was design documentation for all the design components. This explained how each component worked and why it was needed. This is to ensure the web portal is scalable for changes.

Fintech DesignConclusion

As with other industries, there are trends in user behaviours and preferences. Fintech designers must always be aware of market changes and adapt their designs to meet market demands. After all, they are designing for users.

Fintech will stand the test of time, so it can not be merged or erased from the ecosystem. Its relative permanence is a sign for designers to do all they can to remain relevant by learning new technologies and embracing sustainable and human-centric solutions.

FAQs

1. What are the common UX challenges in fintech apps, and how can they be solved?

Fintech apps usually face UX challenges like information overload, complex user flows, poor onboarding, and lack of trust. However, there’s a fix to everything; solutions for these include:

- Simplified user journeys by using intuitive navigation.

- Optimised onboarding with minimal steps and clear instructions

- Built trust with clear, concise, jargon-free communication that reassures data security.

- Not overloading information and using visual hierarchy to avoid confusion among users.

2. Why is accessibility important in fintech apps, and how can it be achieved?

Accessibility in fintech apps refers to apps designed for everyone’s use, with equal importance given to differences in ability, age, gender, and technical knowledge. Accessibility in digital products promotes inclusivity and expands the target audience. It can be achieved through:

- Make sure there is high contrast for text and other interactive elements for people with visual impairments.

- Incorporating features like screen readers’ voice commands are also beneficial.

- The area of touch targets should be large enough for easy navigation.

- Avoiding financial jargon for people who are new to fintech

Let's create something amazing!

Let's discuss your vision and how we can bring it to life with impactful design solutions.

.avif)

Good design starts with Sliced Newsletter

Subscribe to the Sliced newsletter and get the best of research, UX writing, product psychology, CX, and design systems, right in your inbox.